CGR The Value Gap: Sweden

Mining and extraction

The Mining & Extraction sector—ranging from metals and minerals extraction to forestry—plays a foundational role in Sweden’s economy. Sweden’s production of iron ore represents approximately 90-95% of the production in the EU. The country further extracts approximately 265.3 million tonnes of natural resources annually, supported in large part by its vast, actively managed forests, which cover around 70% of the national land area. This abundance makes Sweden an EU as well as global leader in some basic industry sectors. [12]

Mining & Extraction account for approximately 5% of the total Swedish economy.

While the transition to a circular economy may reduce reliance on virgin materials, extraction will remain necessary to meet both current and future demands. Importantly so, for example, for a green transition. As the earliest link in many supply chains, extractive industries provide essential inputs for a range of material- and emissions-intensive sectors. Forest products, for example, are a key input for biofuel production—powering transport and heating systems—and help meet growing demand for bio-based materials in manufacturing.

This sector differs markedly from others examined in this report. Unlike Construction or Agrifood, where consumption is primarily driven by households or government, Mining & Extraction function primarily as a supplier to other industries. To capture this upstream role, the reported consumption figures include intermediate consumption by other sectors. The extractive sector also diverges from the Value Hill framework used elsewhere in the report. Here, processing and distribution play a minimal role, and most waste—and therefore value loss—occurs during extraction, before any consumption takes place. In this context, the concepts of ‘value not created’ and ‘value lost’ overlap. For clarity, the value losses from the sector only include losses from the extraction phase, such as metals left in tailings or other unrecovered materials. These are referred to as end-of-life losses in this context, even though they occur before the production and use stages, differing from how the term is typically used for consumer products.

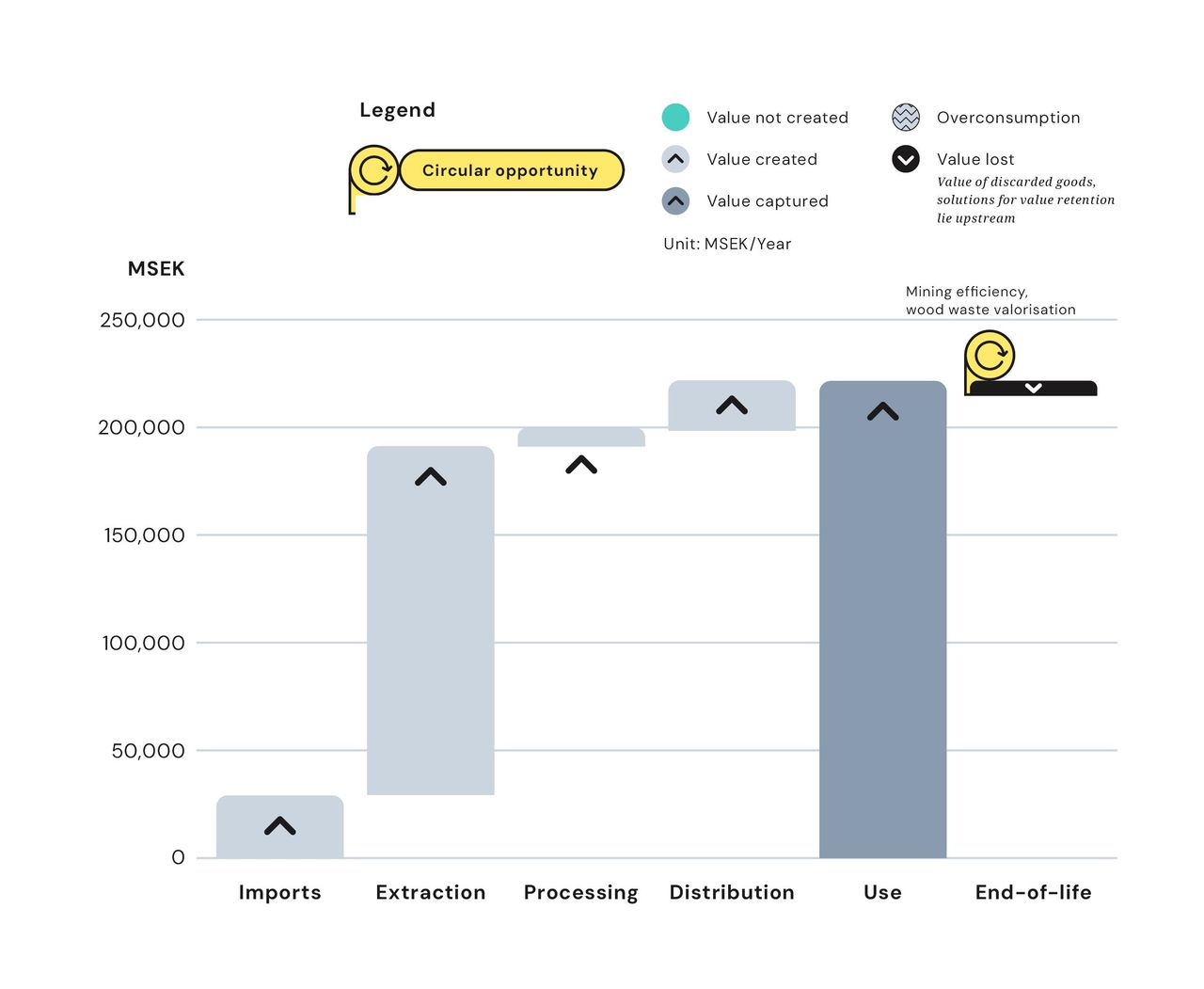

Where value is lost in mining and extraction

As shown in Figure four, Sweden’s Mining & Extraction sector generates approximately SEK 220 billion in consumption value. Of this, an estimated SEK 6 billion—or 3%—is lost at end-of-life, primarily through metals left behind in tailings.

Currently, only SEK 300 million—around 6% of this lost value—is recovered through waste management processes, highlighting a significant opportunity for improved resource recovery.

Unlike other sectors examined in this report, the Mining & Extraction sector operates entirely upstream, providing raw materials that are not yet linked to a specific end use. As such, it does not serve final demand directly and is excluded from the overconsumption analysis. Overconsumption, by definition, applies to sectors where products and services are delivered to end users—typically households or the public sector. In the case of Mining & Extraction, value creation is agnostic to how or where materials will ultimately be used. That said, circular strategies targeting overconsumption in downstream sectors can still have a meaningful impact on extraction. By extending product lifespans, increasing reuse, and reducing material throughput further down the value chain, the demand for newly extracted resources can be significantly reduced

Figure four shows yearly value creation and losses in the Mining & Extraction sector.

Unlocking value through higher yields

The Mining & Extraction sector generates vast quantities of waste—almost 90 million tonnes annually—accounting for roughly 90% of Sweden’s total waste generation, with much of the activity concentrated in remote northern regions. [13] Currently, waste rock and tailings, the two largest waste streams, are not considered economically viable resources, which helps explain why the sector’s identified economic losses appear relatively small today. However, ongoing technological development offers significant potential for future value recovery, suggesting that current low losses primarily reflect limitations in technology and product innovation rather than the absence of recoverable value.

While this analysis does not quantify the potential value from legacy tailings or other waste streams such as waste rock and slags, these represent important opportunities for the mining industry. Emerging research indicates that waste rock could be used for carbon capture, while mine tailings (such as silica) may have applications in civil engineering, [14] unlocking new pathways for resource valorisation. In addition, significant deposits of phosphorus exist alongside iron, copper, zinc, and other valuable minerals, representing further opportunities for value creation.

Beyond mining, the forestry sector also holds substantial potential for higher yields and increased value. Extending forest growth periods, reducing thinning, and replacing small-dimension timber with larger, higher-quality trees can generate greater economic returns. These strategies also enhance carbon storage and support positive biodiversity outcomes, offering benefits that go beyond immediate financial gains.

The Circularity Gap Report is an initiative of Circle Economy, an impact organisation dedicated to accelerating the transition to the circular economy.

© 2008 - Present | RSIN 850278983