CGR The Value Gap: Sweden

Manufacturing

Sweden’s Manufacturing sector includes the production of industrial machinery, steel and metal processing, and the pulp and paper industry. The manufacturing industry is a key driver of the national economy, known for its innovation, efficiency, and sustainability but it’s also a major driver of material demand, consuming 35.7 million tonnes of resources annually—equivalent to 13% of the country’s total material use. [15] This demand fuels significant extraction activity, both domestically and abroad, as raw materials are processed into intermediate and final goods. However, an estimated SEK 13 billion in potential value is lost each year due to energy inefficiencies and material waste during production.

Despite a broader shift toward a more service-based economy in recent decades, [16] Manufacturing remains a cornerstone of Sweden’s economy.

The sector accounts for 22% of total economic output and is pivotal for employment and trade, generating around three-quarters of the country’s export value.

Unlike sectors where consumption is primarily driven by households or the public sector, manufacturing plays a foundational role in supplying other sectors. To reflect this industrial interdependence, this analysis also includes intermediate consumption, capturing the full scope of material and value flows across the Manufacturing cycle.

Where value is lost in manufacturing

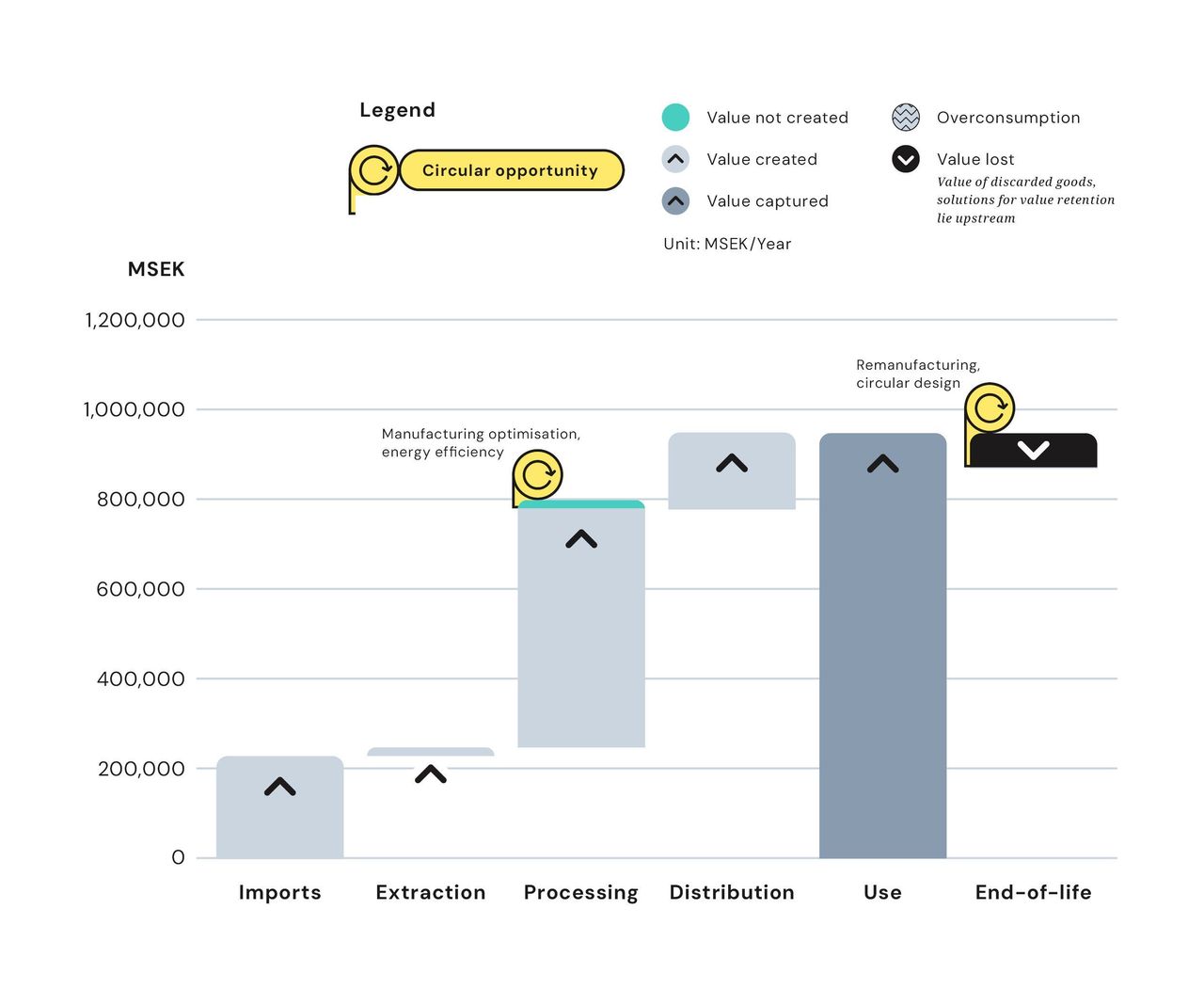

As shown in Figure five, Sweden’s Manufacturing sector generates around SEK 954 billion in consumption value. Yet 9% of this is lost or never created due to linear and inefficient practices, these losses represent both materials and energy lost in the process.

Each year, the sector discards materials and products worth approximately SEK 71 billion, with only SEK 3 billion—or 4%—currently recovered through recycling or other value-retaining processes. This makes the sector a significant point of value erosion in Sweden’s economy.

Unlike sectors that deliver goods and services directly to end users, Manufacturing primarily serves as an upstream supplier to other industries. As such, the concept of overconsumption does not apply in the same way. Similar to the extraction sector, Manufacturing provides intermediate goods not yet tied to specific use or application, and therefore falls outside the scope of end-use-driven overconsumption analysis. Nonetheless, the scale of discarded material highlights the untapped potential for greater circularity and improved resource efficiency across the production process.

Figure five shows yearly value creation and losses in the Manufacturing sector.

Unlocking value through material efficiency, circular design and remanufacturing

The manufacturing sector holds substantial untapped potential for value creation by improving efficiency across the production process. A key opportunity lies in prioritising material efficiency early in the value chain, using innovations that achieve the same functionality and performance with less material—such as lightweight materials—without compromising the technical lifetime of products. This approach not only reduces resource intensity but also streamlines material flows throughout the system.

Reducing scrap and offcuts generated during conventional industrial processes—such as machining, forming, or casting—offers another avenue to enhance operational efficiency and reduce reliance on virgin raw materials. By adopting circular design principles, remanufacturing, and closed-loop recycling, manufacturers can retain more value, lower costs, and contribute to a more resource-efficient economy. Furthermore, developing durable machinery and equipment is essential for advancing Sweden’s circularity while capturing additional value, ensuring that the resources invested in production continue to deliver benefits over the long term.

The Circularity Gap Report is an initiative of Circle Economy, an impact organisation dedicated to accelerating the transition to the circular economy.

© 2008 - Present | RSIN 850278983